According to IHS iSuppli's research, the regulator's growth rate will continue to be faster than the overall analog integrated circuit (IC) market and semiconductor market, and the compound annual growth rate for 2009-2015 will reach 16.0%.

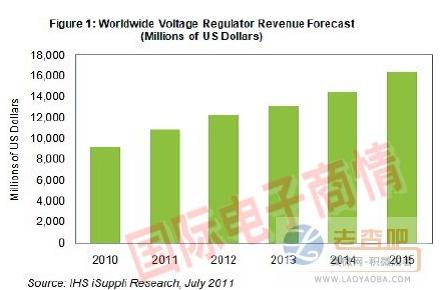

According to IHS iSuppli's research, the regulator's growth rate will continue to be faster than the overall analog integrated circuit (IC) market and semiconductor market, and the compound annual growth rate for 2009-2015 will reach 16.0%. In contrast, the combined annual growth rate of the overall analog IC market and the overall semiconductor market during the same period was 11.9% and 6.3%, respectively. The regulator is a fast-growing market, with sales expected to grow from $9.1 billion in 2010 to $16.3 billion in 2015. The annual growth rate is higher than Other analog IC markets.

The chart above shows IHS iSuppli’s forecast for global regulator sales for 2010-2015.

Leading supplier regulators account for the largest proportion of general-purpose analog IC operating revenue. Therefore, maintaining a strong position in the regulator field will eventually boost the revenue growth of analog IC vendors.

In 2010, Texas Instruments was the leader in this field, with related operating income of 1.7 billion U.S. dollars and a market share of 18.0%. Maxim Integrated Products ranks second with operating revenue of US$936 million and holds a 10.2% share. National Semiconductor’s regulator’s operating revenue was US$758 million, with a share of 8.3%.

The advantage of Texas Instruments is simulation, while ADI is dominant in the field of general-purpose analog ICs. Texas Instruments is the strongest. The company ranked first in three of the four general-purpose analog domains, including regulators, amplifiers, and interface ICs. Overall, TI's general-purpose analog ICs accounted for 57% of its total simulated revenue.

One area where Texas Instruments has not won the top spot is data converters, Analog Devices Inc. (ADI) is the leader in this field. ADI has a 39% share in this area, followed by Texas Instruments with 22%.

Data converters account for 54% of ADI's general-purpose analog IC revenue and 44% of its total semiconductor revenue. Although TI has made progress in narrowing the gap, ADI will dominate the data converter market in the foreseeable future.

Telephone Est Co., Limited , http://www.gd-charger.com